Backdoor Roth IRA and Mega Backdoor Roth IRA Strategies

Introduction

The Roth IRA is a powerful retirement savings vehicle, offering tax-free growth and tax-free qualified withdrawals. However, direct contributions to a Roth IRA are subject to strict income limitations. To circumvent these limits, high-income taxpayers may use the "backdoor Roth IRA" strategy, and, for those with access to certain employer plans, the "mega backdoor Roth IRA." This paper provides a detailed analysis of these strategies, their legal underpinnings, procedures, limitations, and practical considerations.

Legal Framework

Roth IRA Contribution and Conversion Rules

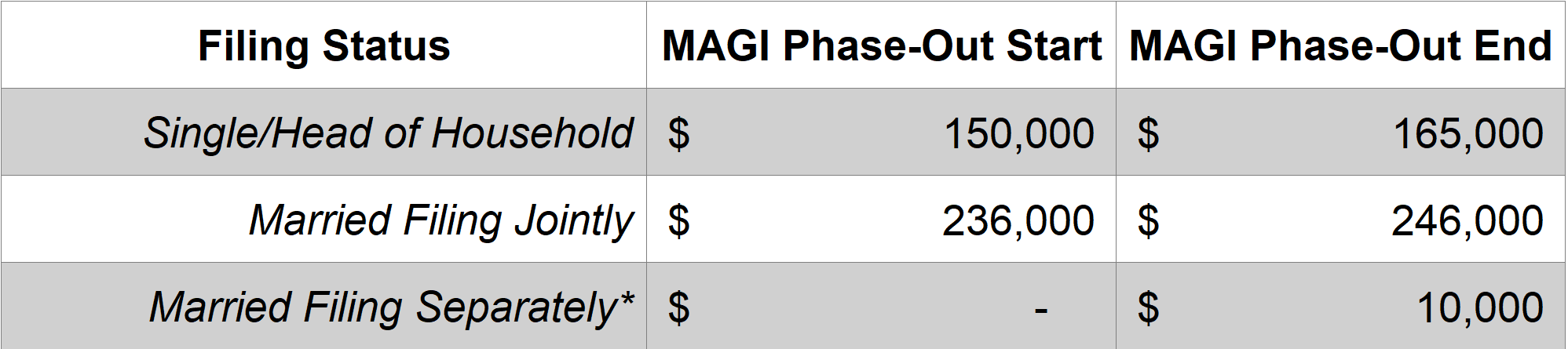

- Direct Roth IRA Contributions: Under IRC § 408A(c)(3), direct contributions to a Roth IRA are phased out and eventually prohibited for taxpayers whose modified adjusted gross income (MAGI) exceeds certain thresholds. For 2025, the phase-out for single filers is $150,000–$165,000 and for married filing jointly is $236,000–$246,000.

- Traditional IRA Contributions: Anyone with earned income can contribute to a traditional IRA, subject to annual limits ($7,000 for 2025, plus $1,000 catch-up if age 50+).

- Roth IRA Conversions: There are no income limits on converting traditional IRA assets to a Roth IRA. This was established by the Tax Increase Prevention and Reconciliation Act of 2005, effective 2010.

Step Transaction Doctrine and Substance-Over-Form

- The step transaction doctrine, a subset of the substance-over-form doctrine, can collapse a series of steps into a single transaction if the steps are interdependent and intended to achieve a result not permitted directly.

- Recent case law (e.g., Summa Holdings, Benenson) and IRS commentary suggest that, when each step is independently authorized by statute and has economic and legal effect, the doctrine does not apply to recharacterize a backdoor Roth IRA as an impermissible excess contribution.

Procedures

Step 1: Make a Nondeductible Traditional IRA Contribution

- Contribute up to the annual limit ($7,000 for 2025, plus $1,000 catch-up if age 50+) to a traditional IRA.

- The contribution is nondeductible if the taxpayer is covered by a workplace plan and exceeds the MAGI limit for deductibility.

Step 2: Convert the Traditional IRA to a Roth IRA

- Convert the entire traditional IRA balance to a Roth IRA.

- If the traditional IRA contains only the recent nondeductible contribution, little or no tax is due on conversion.

- If the taxpayer has other pre-tax IRA balances, the pro rata rule applies, and a portion of the conversion will be taxable.

Timing: There is no statutory waiting period between the two steps, but some practitioners recommend waiting at least a few days or a statement period to ensure the steps are respected as separate transactions.

Mega Backdoor Roth IRA

Eligibility: Only available to participants in 401(k) plans that allow after-tax (non-Roth) contributions and in-service withdrawals or in-plan Roth conversions.

Step 1: Make After-Tax Contributions to 401(k)

- Contribute after-tax dollars to the 401(k) plan, up to the overall annual addition limit ($70,000 for 2025, including employee deferrals, employer contributions, and after-tax contributions).

Step 2: Convert or Rollover After-Tax Contributions

- Convert the after-tax contributions to a Roth 401(k) account within the plan (in-plan Roth conversion) or roll them over to a Roth IRA.

- The conversion or rollover is generally not taxable, except for any earnings on the after-tax contributions.

Income and Contribution Limitations

Roth IRA Direct Contribution Limits (2025)

*If lived with spouse at any time during the year

Traditional IRA Contribution Limits (2025)

- $7,000 per person ($1,000 catch-up if age 50+)

- Deductibility phases out for those covered by a workplace plan at higher MAGI levels, but nondeductible contributions are always allowed if there is earned income.

401(k) and Mega Backdoor Roth Limits (2025)

- Employee elective deferral: $23,500 ($7,500 catch-up if age 50+)

- Total annual additions (employee + employer + after-tax): $70,000

- After-tax contributions are only possible if the plan allows, and the sum of all contributions cannot exceed the annual addition limit.

Pros and Cons

Pros

Backdoor Roth IRA:

- Allows high-income taxpayers to fund a Roth IRA despite income limits.

- Enables tax-free growth and tax-free qualified withdrawals.

- No required minimum distributions (RMDs) during the account owner’s lifetime.

Mega Backdoor Roth IRA:

- Allows much larger Roth contributions (up to $70,000 in 2025, less other contributions).

- Accelerates Roth savings for those with high savings capacity and access to a suitable 401(k) plan.

Cons

Backdoor Roth IRA:

- The pro rata rule: If the taxpayer has other pre-tax IRA balances, a portion of the conversion will be taxable.

- Complexity in tracking basis and reporting on Form 8606.

- Potential for IRS scrutiny, though recent case law and IRS commentary support the strategy.

Mega Backdoor Roth IRA:

- Not all 401(k) plans permit after-tax contributions or in-service withdrawals/conversions.

- Plan rules may limit the ability to execute the strategy.

- Requires careful coordination to avoid exceeding annual limits.

Workplace Qualified Plan Limitations

- Backdoor Roth IRA: No direct impact from workplace plans, except that participation in a workplace plan may limit the deductibility of traditional IRA contributions, but not the ability to make nondeductible contributions.

- Mega Backdoor Roth IRA: Only available if the employer’s 401(k) plan allows after-tax contributions and in-service withdrawals or in-plan Roth conversions. Plan documents and administrative practices vary widely.

Other Caveats and Considerations

Pro Rata Rule

- When converting to a Roth IRA, all traditional, SEP, and SIMPLE IRAs are aggregated for tax purposes. The ratio of after-tax to pre-tax dollars determines the taxable portion of the conversion.

Timing and Step Transaction Doctrine

- While there is no statutory waiting period, some practitioners recommend waiting a few days or a statement cycle between the traditional IRA contribution and Roth conversion to reinforce the separateness of the steps.

- Courts have generally respected the backdoor Roth IRA when each step is independently authorized and has legal effect.

Reporting Requirements

- Form 8606 must be filed to report nondeductible IRA contributions and to track basis.

- The conversion is reported on Form 1099-R and Form 1040.

Early Withdrawal Penalties

- Withdrawals of converted amounts from a Roth IRA within five years may be subject to a 10% penalty unless an exception applies.

Conclusion

The backdoor Roth IRA and mega backdoor Roth IRA are powerful tools for high-income individuals to achieve tax-free retirement savings. While both strategies are currently supported by the Internal Revenue Code, case law, and IRS commentary, they require careful attention to procedural details, plan rules, and reporting requirements. Practitioners should remain vigilant for legislative changes and ensure clients understand the potential risks and benefits.

For personalized assistance, detailed analyses, and ongoing support:

Schedule Your Consultation

Learn More About Our Specialized Services

Connect Directly with Levon Galstian

Published By:

SMB CPA Group, PC